Positive earnings fuel strong demand for shares

KUWAIT: Boursa Kuwait ended last week in the green zone. The Price Index closed at 6,807.90 points, up by 0.76 percent from the week before closing, the Weighted Index increased by 1.04 percent after closing at 414.42 points, whereas the KSX-15 Index closed at 957.33 points up by 0.92 percent. Furthermore, last week's average daily turnover increased by 18.55 percent, compared to the preceding week, reaching KD 12.74 million, whereas trading volume average was 75.59 million shares, recording an increase of 22.14 percent.

The trading activity during the last week, which was limited to three sessions only, revealed green closing zone to the three indices, in light of the noticeable purchasing activity on some leading and operational stocks, especially the ones that disclosed good annual results and distributions for the last financial year, in addition to the quick speculative operations that included some small-cap and idle stocks. Such performance came amid an increased daily trading averages compared to the preceding week, whereas the average cash liquidity increased by 18.55 percent to reach KD 12.74 million, while the average number of traded stocks during the week increased by 22.14 percent, reaching 75.59 million stock.

Also, last week witnessed trading activity on 138 stock out of 176 listed stock in the Market, whereas 56 stock prices increased and 58 stock prices decreased, and 62 stock remained with no change.

On the other hand, the market capitalization for Boursa Kuwait during the last week increased by around KD 322.30 million, compared to its level in a week earlier, as it reached by the end of the week around KD 27.54 billion against KD 27.22 in the preceding week, with a growth of 1.18 percent. The market cap gains for Boursa Kuwait reached since the beginning of the year to date around KD 602.31 million, up by 2.24 percent compared to its value at end of 2017, where it was KD 26.94 billion. (Note: The market cap for the listed companies in the primary market is calculated based on the average number of outstanding shares as per the latest available official financial statements).

Moreover, Boursa Kuwait initiated its first session of the week with good gains to its three indices, especially the Weighted and KSX-15 indices which benefited from the active trading that concentrated on the leading and heavy stocks, the biggest supporter to the Market during the current period. The Market realized such gains in parallel with the trading indices growth of both the value and the volume, whereas the cash liquidity increased by the end of the session by around 40 percent, reaching about KD 15 million, while the volume grew by about 57 percent during the session reaching around 78 million stock.

On the next session, the Market performance did not change much, as the three indices ended the session's trading with mixed gains, supported by the continued purchasing activity that concentrated on the leading stocks, especially in the Banks sector that acquired 60 percent of the total Market cash liquidity, which reached around K.D. 12 million by the end of the session. On the end of week session however, the Market witnessed a fluctuated performance, whereas the Price and Weighted indices were able to increase by the end of the session supported by the continued presence of the purchasing operations executed on some small-cap and mid-cap stocks, while KSX-15 Index recorded a limited decline by the end of the session, affected by the profit collection operations executed on some heavy stock, however, it was not enough to push the Index towards the red zone on the weekly level.

For the annual performance, the Price Index ended last week recording 6.24 percent annual gain compared to its closing in 2017, while the Weighted Index increased by 3.24 percent, and the KSX-15 recorded 4.64 percent growth.

Sectors' Indices

Five of Boursa Kuwait's sectors ended last week in the green zone, five recorded declines, whereas the Health Care sector's index & Technology sector's index closed with no change from the week before. Last week's highest gainer was the Financial Services sector, achieving 2.35 percent growth rate as its index closed at 625.89 points. Whereas, in the second place, the Industrial sector's index closed at 1,876.52 points recording 1.15 percent increase. The Consumer Goods sector came in third as its index achieved 0.59 percent growth, ending the week at 814.70 points.

On the other hand, the Telecommunications sector headed the losers list as its index declined by 1.11 percent to end the week's activity at 537.10 points. The Consumer Services sector was second on the losers' list, which index declined by 0.84 percent, closing at 864.28 points, followed by the Basic Matrials sector, as its index closed at 1,299.56 points at a loss of 0.35 percent.

Sectors' Activity

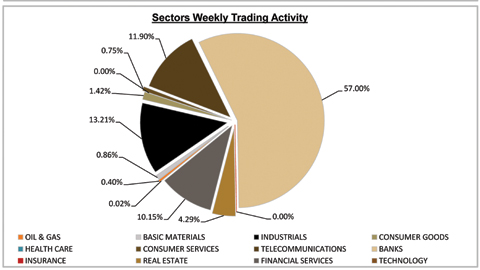

The Banks sector dominated a total trade volume of around 91.07 million shares changing hands during last week, representing 40.16 percent of the total market trading volume. The Financial Services sector was second in terms of trading volume as the sector's traded shares were 20.65 percent of last week's total trading volume, with a total of around 46.84 million shares.

On the other hand, the Banks sector's stocks were the highest traded in terms of value; with a turnover of around KD 21.78 million or 57 percent of last week's total market trading value. The Industrial sector took the second place as the sector's last week turnover was approx. KD 5.05 million representing 13.21 percent of the total market trading value. -- Prepared by: Studies & Research Department - Bayan Investment Co.

BAYAN WEEKLY MARKET REPORT