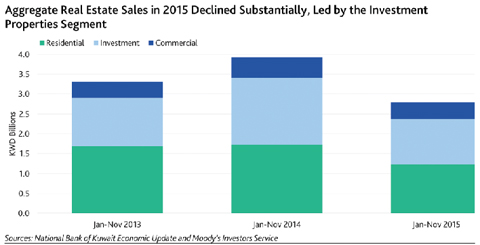

KUWAIT: Last Wednesday, a Kuwait International Bank report showed a significant 29% decline in Kuwait's (Aa2 stable) 2015 real estate sales amid softening prices, suggesting low sales volumes and lower real estate values in 2016. A decline in real estate sales would adversely affect banks' new business volumes and earnings. A decline in real estate values would increase credit risks for Kuwaiti banks that are highly exposed to real estate through collateral. More granular data show that by November 2015 all major real estate segments suffered declines in aggregate sales after several years of strong performance and a record year in 2014, with investment property sales declining 32% year-on-year - more than other segments, as shown in the exhibit below.

KUWAIT: Last Wednesday, a Kuwait International Bank report showed a significant 29% decline in Kuwait's (Aa2 stable) 2015 real estate sales amid softening prices, suggesting low sales volumes and lower real estate values in 2016. A decline in real estate sales would adversely affect banks' new business volumes and earnings. A decline in real estate values would increase credit risks for Kuwaiti banks that are highly exposed to real estate through collateral. More granular data show that by November 2015 all major real estate segments suffered declines in aggregate sales after several years of strong performance and a record year in 2014, with investment property sales declining 32% year-on-year - more than other segments, as shown in the exhibit below.

"Investment property" is an official classification in Kuwait for apartments that are typically rented out and provide income to landlords. We attribute the slowdown in this sector partly to reduced investor interest amid low oil prices. It has not yet affected real estate companies: listed companies' aggregate profits were up 7% year-on-year for the first nine months of 2015. However, further pressures in 2016 will adversely affect the sector's revenues and likely drive prices down.

Real-estate-related lending drove banks' growth for the past several years and the real estate sales slowdown reduces growth prospects. Between year-end 2008 and 2014, the compound annual growth rate of real estate and installment loans (ie, long-term personal loans for the repair and purchase of private homes ) was a high 8.1%, compared to 4.5% growth in total domestic loans. Declining real estate prices in 2016 will also increase credit risks for Kuwaiti banks, which are highly exposed to the sector.

According to the Central bank of Kuwait, as of September 2015, 25% of banks' domestic loans were to the real estate sector, while a further 28% were installment loans to individuals. Furthermore, around 40% of banks' total loan collateral is linked to real estate. The sector was one of most severely affected in the wake of the global financial crisis in 2007-08 and banks' asset quality experienced significant impairment.

Nonetheless, Kuwaiti banks are now better positioned to withstand higher impairments from potential shocks in the real estate market. At the end of 2014, Basel III Tier 1 ratios were 14.8% on average for rated banks. We also expect capitalisation will continue to improve because the Central Bank of Kuwait is conservatively introducing Basel III capital requirements that are 2.5 percentage points higher than Basel recommendations. Rated banks in Kuwait also maintain a high level of general provisions, equivalent to 3.6% of gross loans as of year-end 2014, because the central bank has been requiring banks to book substantial precautionary provisions against performing loans.

The central bank has also taken various macro-prudential measures to address the resurgence of real-estate related risks. In late 2013, it issued guidelines on loans for purchasing and/or developing real estate. These guidelines include loan-to-value ceilings of 50% for the purchase of undeveloped land, 60% for the purchase of existing real estate and 70% for construction purposes. Together with the initial implementation of Basel III capital requirements, the central bank also issued regulations in December 2014 where the previous treatment of real estate collateral as a risk mitigant in the calculation of risk-weighted assets (RWAs) is to be phased out. In the past, banks could use 50% of the value of real estate collateral as a discount against relevant RWAs. The elimination of this discount, by 10% yearly over five years, will gradually increase RWAs, forcing Kuwaiti banks to hold higher capital buffers against real estate exposures. -- Credit Outlook