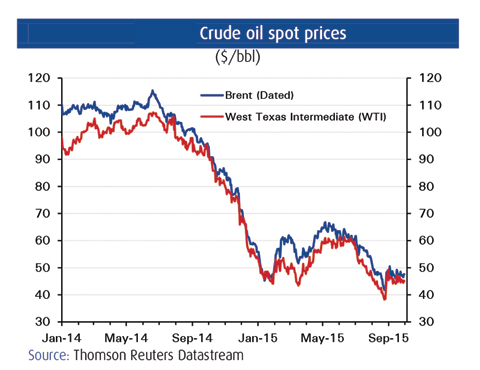

KUWAIT: The volatility that characterized oil markets in late August gave way to a more settled period in September, with benchmark crudes, Brent and West Texas Intermediate (WTI), trading within the $46-49.0 per barrel (bbl) and $44-46.0/bbl ranges, respectively, for most of the month. At September's close, Brent settled at $47.2/bbl while WTI reached $45.1/bbl. Both crudes were still down near six-and-a-half-year lows, however, depressed by continued worries about economic growth in emerging markets, particularly China's, and by the persistence of the crude oil supply glut. The US Federal Reserve's decision to hold interest rates steady was partly an implicit acknowledgment of the former, while the supply overhang dynamic was further evident in the rise to record levels of OECD commercial oil stocks and continued price discounting by regional oil producers Kuwait and Iran. The current discount of Kuwaiti export crude (KEC) against Saudi Arabia's benchmark Arab Light for Asian customers is the largest in 10 years as efforts intensify even among OPEC members to retain market share.

KUWAIT: The volatility that characterized oil markets in late August gave way to a more settled period in September, with benchmark crudes, Brent and West Texas Intermediate (WTI), trading within the $46-49.0 per barrel (bbl) and $44-46.0/bbl ranges, respectively, for most of the month. At September's close, Brent settled at $47.2/bbl while WTI reached $45.1/bbl. Both crudes were still down near six-and-a-half-year lows, however, depressed by continued worries about economic growth in emerging markets, particularly China's, and by the persistence of the crude oil supply glut. The US Federal Reserve's decision to hold interest rates steady was partly an implicit acknowledgment of the former, while the supply overhang dynamic was further evident in the rise to record levels of OECD commercial oil stocks and continued price discounting by regional oil producers Kuwait and Iran. The current discount of Kuwaiti export crude (KEC) against Saudi Arabia's benchmark Arab Light for Asian customers is the largest in 10 years as efforts intensify even among OPEC members to retain market share.

Meanwhile, in the futures markets, the price for long-dated crude oil continues to trade higher than spot crude (i.e. crude for immediate delivery). (Chart 2.) The differential between the two prices in the so-called contango curve has narrowed, however, indicating that the appetite for storage for speculative purposes may be waning. As of September 30, according to the futures market, the price of Brent crude is expected to increase to $55.2/bbl by December 2016 and to $58.6/bbl by December 2017.

Crude supply glut should ease in 2016 as oil demand rebounds and oil supply begins to be negatively affected by low oil prices

The expectation that oil prices will rebound going into 2016 and beyond is based on a predicted unwinding of the demand/supply mismatch. The oil supply glut, which the International Energy Agency (IEA)estimated to be around 1.6 million barrels a day (mb/d) during the third quarter of this year (3Q15), should begin to ease as demand rebounds from the lows of 2014 and supply growth slows due to cuts in investment and ultimately production due to low oil prices.

Looking ahead, the current oil surplus could steadily decline and turn into a deficit of almost -0.5 mb/d by 4Q16 (Chart 4.) as oil demand growth outpaces oil supply growth. On the demand side, 2015 should see demand rising to a five-year high of 1.7 mb/d before moderating in 2016 to 1.4 mb/d. Preliminary estimates for 3Q15 show that demand growth topped 1.7 mb/d for the third quarter in a row, boosted by better-than-expected numbers from the US, China, Europe and Russia. (Chart 5.) Improving macroeconomic fundamentals, baseline revisions in the US and still strong demand from China's petrochemical and transport sectors helped keep demand firm. Underpinning this trend is the stimulative effect on crude oil demand of lower oil prices

Conversely, low oil prices are having a negative effect on global supplies, especially on non-OPEC crude oil production. According to the IEA, non-OPEC supply growth, having peaked in 4Q14 at 2.6 mb/d,is expected to slow considerably, to -0.3 mb/d by the end of the year before bottoming out at -0.9 mb/d at the end of 2Q16. For 2015 as a whole, the IEA expects non-OPEC supply growth to slow to 1.1 mb/d, from 2.3 mb/d last year. In 2016, non-OPEC supply growth is projected to contract by 0.5 mb/d. The IEA anticipates that a significant portion of this will be due to declines in US light tight oil production (LTO) i.e. shale. With oil prices below the estimated breakeven cost for major US shale plays, the decline in drilling and completion rates that has been observed since the start of the year is expected to extend well into 2016.

OPEC output, meanwhile, at 31.9 mb/d in August, remains elevated near the 22-month high recorded in July and well above the group's official production ceiling of 30 mb/d. Production has surged by more than 1.5 mb/d year-on-year (y/y) even while prices have fallen by more than 50% over the same period. Compared to July, however, OPEC production did decline by 20,000 b/d on slightly lower output from Saudi Arabia, the UAE and Angola among others. Nevertheless, Saudi Arabia, along with the UAE and Iraq, continues to pump at or near record levels. Saudi Arabia's output of 10.2 mb/d in August was the sixth in a row to top 10.0 mb/d, suggesting that the kingdom remained steadfast in its pursuit of market share. Elevated output was also in response to heightened domestic power demand during the hot summer months.

Iraqi production, which includes output from the Kurdistan Regional Government's (KRG) oil fields, hit another all-time high, of 3.76 mb/d, in August. Output has surged despite the conflict with Islamic State (IS) and plunging oil prices.

Kuwait, meanwhile, boosted oil production by 70,000 b/d to 2.89 mb/d, according to official sources. This was the highest figure in a year, and resulted from the successful application of enhanced oil recovery (EOR) techniques to the country's maturing fields. Otherwise, output could conceivably be down by at least 250,000 b/d in view of the cessation of production from both the Khafji and Wafra oil fields that Kuwait shares with Saudi Arabia in the Neutral Zone. The two countries have yet to resolve the operational dispute that shuttered production.

For the third month in succession, Iranian production edged up in August, to 3.18 mb/d. Iran is preparing the ground for a full return to the oil markets in early 2016 when sanctions are expected to be lifted. Iran expects output to rise by 500,000 b/d as soon as sanctions are removed and by 1.0 mb/d within months. Many observers view this figure as optimistic, however.

Iran's return to the oil markets in 2016 amid the persistent supply glut that has forced down prices is likely to dominate proceedings at OPEC's next meeting in December. It remains to be seen whether the group will accommodate Iran by lowering individual quotas or continue with its Saudi-led strategy of resisting production cuts in the interests of preserving market share.