Downside risks include US shale gains and end to OPEC+ supply curbs

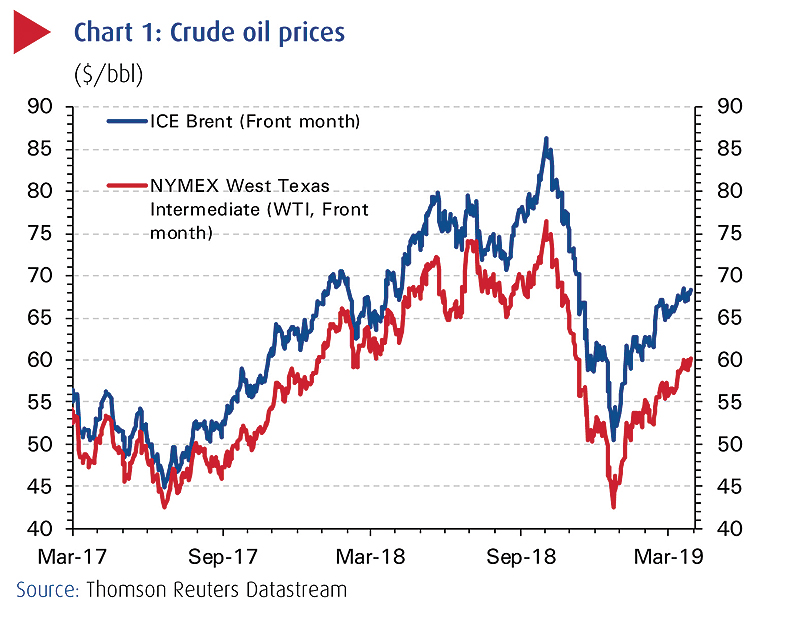

KUWAIT: Oil prices closed out March with their best quarterly performance since 2009, with Brent and WTI rising by 27 percent and 32 percent, respectively, in 1Q19. Benchmark Brent crude ended March at $68.4/bbl, having traded sideways in the $66-68 range for most of the month. The US marker, West Texas Intermediate (WTI), hit $60 last week for the first time since November 2018.

Oil prices have been buoyed by signs that the market is tightening, with Saudi Arabia, especially, taking the lead in cutting oil production aggressively to drain any excess supply that could put downward pressure on the price . Russia, its non-OPEC partner, also recently reaffirmed its commitment to the Vienna Agreement by indicating that it was on track to meet its quota obligation by the end of March or the beginning of April. Furthermore, OPEC's efforts have been augmented by falling output from Iran and Venezuela due to political turmoil, mismanagement and US sanctions as well as by lower supplies from Canada and Libya. Iranian production was down 28 percent y/y at 2.74 mb/d in February, according to OPEC secondary sources, while its exports over the same period were almost halved to 1.3 mb/d, Bloomberg reported. In Venezuela, crude production was at around a 28-year low of of 1.0 mb/d in February, according to OPEC data.

Even in the US, the data has been less bullish of late. While US crude production continues to break new ground, reaching 12.1 mb/d in the week-ending 22 March, the number of oil drilling rigs has fallen for six consecutive weeks, by a cumulative 69, or 7.8 percent in 2019 to 816, according to Baker Hughes.

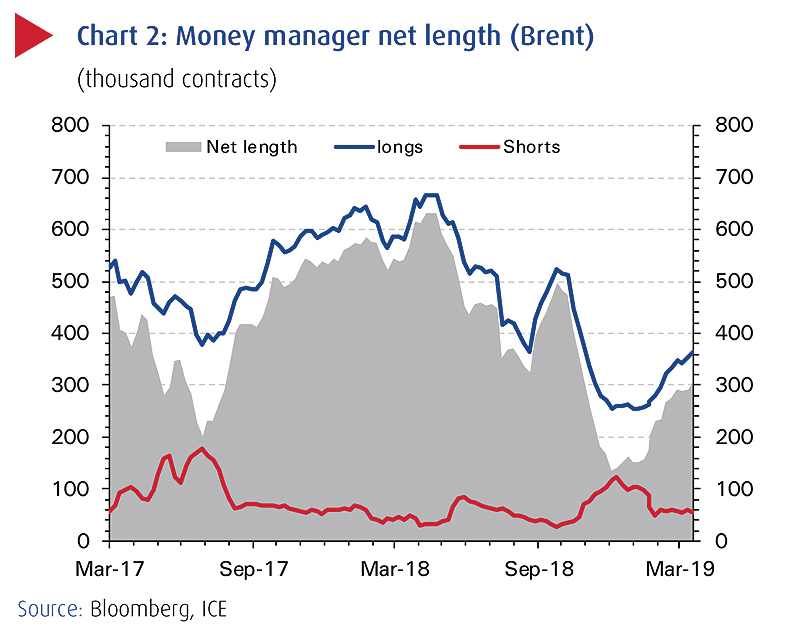

As a measure of market optimism, hedge fund managers have increased wagers on oil prices rising to the highest since October 2018. Money manager net length (the ratio of long to short positions) reached 308,606 combined futures and options contracts as of 19 March.

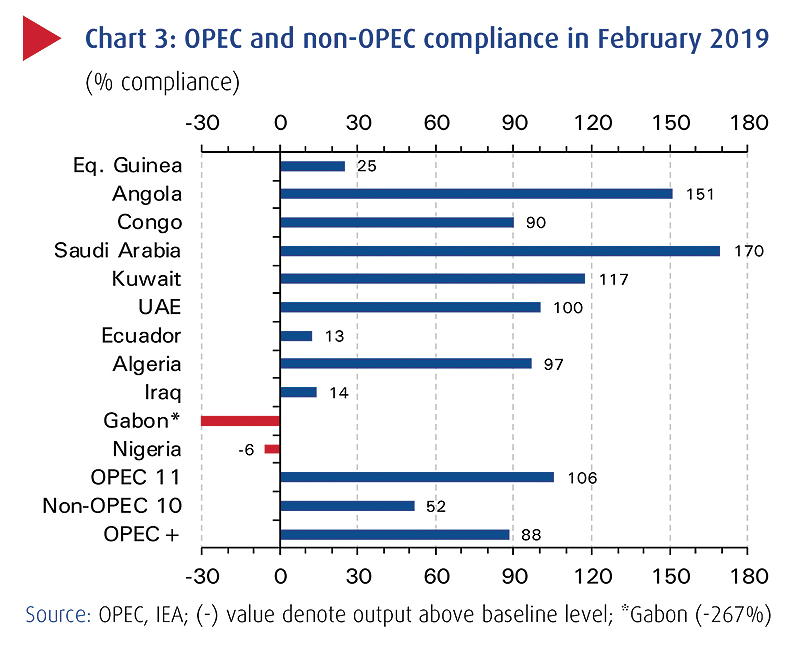

Led by Saudi Arabia, which appears determined to prop up oil prices (allegedly targeting $70 barrel), OPEC-11 compliance (Iran, Venezuela and Libya are excluded) reached 106 percent in February, with aggregate production falling by 812 kb/d from the Vienna Agreement partners' reference level to 25.9 mb/d (30.6 mb/d for OPEC-14). GCC oil exporters Saudi Arabia and notched up a second consecutive month of overcompliance, while the UAE reached its production quota target for the first time. Non-OPEC compliance, meanwhile, improved to 52 percent in February from 25 percent in January. Russia reiterated last week that it intends to fully comply soon.

Oil supply/demand balances indicate tighter market

The International Energy Agency (IEA) has left unchanged its global oil demand growth estimate for 2019 at 1.4 mb/d, a slight increase on 2018's estimate of 1.3 mb/d, but with a synchronized global growth slowdown, this could be revised down. Assuming that OPEC-11 continues on its current trajectory of overcompliance (and production in Iran/Venezuela/Libya stays at February levels) and factoring in the IEA's projection for non-OPEC supply growth of 1.8 mb/d this year, then the demand/supply balance should flip into a deficit over 2Q-3Q19. It should then revert back to a slight surplus in 4Q19.

Oil prices might be expected to thus firm up over 2Q-3Q19, which seems to be the consensus at the moment. Of course, the oil price outlook rests on several moving parts, not all of which will come into play to the extent envisaged or at all during the remainder of the year. Of those that could affect prices positively, the expiration and non-renewal of the 180-day US sanctions wavers on Iran in early May might be expected to have the greatest impact, possibly shaving another few hundred thousand barrels per day off global crude supply. But it is not clear yet what the Trump administration intends to do in this regard.

On the one hand, Trump will want to honor his pledge to be tough on Iran but on the other he will want to keep gasoline prices low for the US consumer and to improve his re-election chances in 2020. A more aggressive response vis-à-vis Iran in the context of falling Venezuelan production could lead to an even tighter market, especially in heavy crude, and propel crude prices above what the president would be comfortable with. Extending the waivers for another six months or slowly tightening the criteria, by reducing the list of countries eligible for waivers, for instance, might be an attractive middle way.

Quarterly oil demand and supply balance in 2019

Downside risks to oil prices could include: (i) greater-than-expected US shale-led supply gains; (ii) termination of the OPEC+ supply agreement in June, or under-compliance by a few members; and (iii) a further weakening of global economic growth. The former is looking less likely at the moment, however, with reports of pipeline blockages in Texas, slowing-to-stalling average monthly production, and a sixth-consecutive week of declining rig counts. Indeed, in early March the US Energy Information Administration (EIA) cut both its 2019 and 2020 oil production forecasts, by 110 kb/d to 12.3 mb/d in 2019 and by 170 kb/d to 13.03 mb/d in 2020, respectively. Drilling in the smaller shale plays has become more circumspect amid a focus on shareholder returns.

Enter the IMO 2020 regulations as the wildcard

Looming over the horizon is the International Maritime Organization's (IMO) 2020 regulations on ships' sulfur emissions. These will come into force on 1 January 2020 and require all ships to reduce sulfur dioxide emissions from 3.5 percent to 0.5 percent. To comply, ships will be forced to switch from high sulfur fuel oil (HSFO)-which are among the residual products of the refining process-to low sulfur diesel/gasoil or install scrubbers to remove the sulfur.

Demand for oil from maritime shipping accounts for 3 percent of the market (5 mb/d), and the phasing out of HSFO is expected to put upward pressure on diesel prices and crude oil prices indirectly in late 2019 and early 2020. But the oil price impact could be asymmetrical, with upward price pressure on light sweet crudes such as Brent, which are low in sulfur, and downward pressure on heavier sour crudes such as Dubai and Iraqi crudes, which yield higher levels of sulfur in comparison. Much will depend on how prepared global refineries are for the change, and it may take until 2H19 for the situation to become clearer.

NBK OIL MARKET COMMENTARY